The functional expenses are listed as functional and reported in their Functional Expenses Statement. Non-profit organizations most widely use this form of reporting expenditure.

The functional expenses are listed as functional and reported in their Functional Expenses Statement. Non-profit organizations most widely use this form of reporting expenditure.

Here are several important concepts of non-profit accounting to help you understand functional cost:

- What Are Functional Expenses?

- Functional Classifications vs Natural Classifications

- Statement of Functional Expenses Example

- What Is Functional Expense Allocation?

- What Financial Statements Do Nonprofits Issue?

What Are Functional Expenses?

Their functional classification is a report on functional expenses. Following the Financial Accounting Standards Board requirements, all non-profit organizations in the US now have to declare their expenditures according to their practical classification and their natural classification.

What are functional expenses and natural costs? You will see this: functional expenditures specify the purpose of the spending by type, while natural classifications describe the expenditure.

Functional Classifications vs. Natural Classifications:

Non-profit corporations record both functional and natural expenses. According to these functional levels, businesses report expenditures:

Programs:

Program costs shall be any costs associated with managing a non-profit organization’s numerous programs and facilities per the purpose. Program expenses also account for more of the net costs of existing non-profits.

Management and General:

Management and general expenses support spending related to financing the organization’s daily operations. Such expenses don’t apply to the non-profit mission, which typically includes costs such as administration, bookkeeping, and governance.

Fundraising:

The fundraising cost is the sponsorship of expenditures related to a charitable support or cash support call for an organization. This will cover the expenditures involved with fundraiser activities, direct mail campaigns demanding contributions, and fundraising staff compensation.

Organizations also apply their natural classification costs, which may include:

Salaries, Office rent, Insurance, Utilities, Repairs, Office supplies, and Depreciation.

The Functional Expenses Statement representing non-profit is called a matrix because entities must record their expenses through both functional and natural classifications.

Non-profit accounting is separate from corporate accounting, as no non-profits work to make a profit. Instead, they carry out activities that discuss particular needs in our community.

Nonprofits must learn how to record functional expenses correctly to ensure compliance with federal regulations.

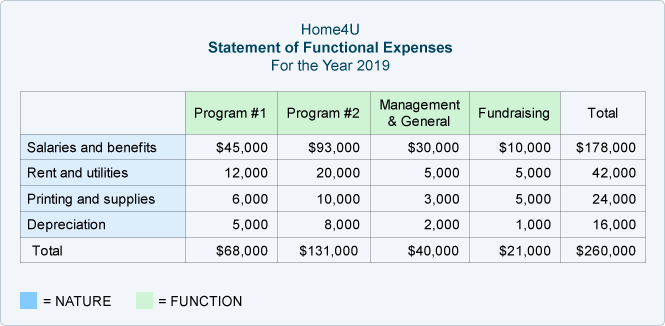

Statement of Functional Expenses Example:

The report of functional expenses is defined as a matrix because it represents their function expenses (programs, management, and general funding) and their nature or form of expense (salaries, rent).

Compiling a Statement of Functional Expenses for a non-profit organization may sound complicated because it entails reporting costs in two categories. This is an example of an accounting coach’s statement of functional expenses to show you how this statement works:

We highlighted the column headings for learning purposes, showing expenses by function. In the first column, we have highlighted the words as they reflect the essence or expenses.

What Is Functional Expense Allocation?

Operating expenses distribution involves the system by which an accountant or bookkeeper of a non-profit entity classifies each cost according to its functional classification. For Non-profit organizations, it is necessary to report their expenditures by role to help understand the functional distribution of expenses.

The audience of a financial reporting company includes financing organizations, donors, governing boards, and regulators. These stakeholders reflect on the relationship between program expenses and funding costs in a non-profit organization. They want to know how the supporting expenses of a company influence and control its programs.

The division of functional expenses tells the stakeholders in an organization that its natural expenditures continue to sustain the organization’s activities and resources.

For functional expenses, there are various allocation strategies, including:

- Square Feet: Costs may be allocated on the basis of square footage occupied by the departments of an organization for natural expenses like rent and utilities. For instance, a non-profit organization might equate its overall square footage to the square feet occupied by its fundraising department. The disparity will allow a company to assess the proportion of its rent to collect funds.

- Headcount: It is always simpler for small companies or those with remote workers, based on headcount, to invest. To do so, the percentage of people who work on each program is expended.

- Time Studies: Certain businesses determine that every employee reports the amount of time they spend in a pay period. The non-profit then measures the total time each worker spends on his programs, administration, and collection of funding. These records will then be used periodically to distribute costs.

- Direct Costs: Certain costs only apply to one form of classification under a given program, for instance, grant payments. These expenses can be explicitly distributed.

What Financial Statements Do Nonprofits Issue?

Non-profit organizations issue financial statements that vary from corporate financial statements. The following financial statements were made for non-profit organizations:

Statement of Financial Position:

In the non-profit sector, the financial statement has a similar position to a company’s balance sheet. The Financial Statement lists all the debt’s values and valuation due to all the company’s properties. It also contains non-profit net assets, which display the organization’s total worth, equivalent to the business’s equity.

Statement of Functional Expenses:

The Statement of Functional Expenses contains information on the expenses incurred for each area of the company. The classifications include programs, management and general, and collection of funds.

Statement of Activities:

The statement of activities is close to the dilemma of the company’s income statement. The Statement of Activities encompasses the company as a whole and focuses on non-profit revenues and expenditures over a given accounting period.

Statement of Cashflows:

The Statement Of Cash Flows reports about all cash flows to and from Nonprofit organizations. The statement reveals how much revenue the programs and activities of the organization produce and utilize.

For more useful information, browse the resources guide today!

Related Articles: