The income Statement is also known as the Profit and Loss Statement. It is one of the Financial Reports prepared by a business; the other two reports are the Balance sheet and Cashflow statement.

The income statement represents a company or business’s profit for a specific period. A business/company prepares an income statement by setting a time frame such as current month, quarter, or annual/yearly financial data.

To prepare an income statement or profit and loss report, you have to follow these steps:

- Create a trial balance standard report. You can take a printout from software, etc.

- Determine the revenue line and place it in the revenue line, which is the first line in the income statement.

- Determine the cost of goods sold and place it under the line of revenue.

- Now deduct the cost of goods sold from the revenue amount and calculate the gross profit.

- Calculate operating expenses.

- Calculate income.

- Apply the tax rate on income.

- Calculate net income.

- Now, finalize the income statement by adding headers about business details, the reporting period, etc.

These steps are summarized above and will be discussed in detail in the next part of the article.

These topics will show you how to prepare an income statement:

- How to write an Income Statement?

- Example Of Income Statement

- Difference between a balance sheet and an income statement

How to write an Income Statement?

To write an income statement representing the profitability of your business, you have to take the following steps:

Choosing a reporting time period:

Firstly you have to choose a financial reporting period on which you want to prepare an income statement for your business. Businesses usually prepare their income statements monthly, quarterly, or yearly. Large companies/businesses report quarterly, but small companies do not need to apply restrictions while reporting. Reporting every month helps a business to know its expenditures and profitability over the period. When the business overlooks its expenditures and profits, it can easily make its business more efficient and profitable.

Print a trial balance report:

You will have to print a trial balance standard report from a specific software your business uses to calculate your income. The trial balance document is an internal document used for reporting ending balances in general ledgers form to help you create your income statement.

Determine Revenues:

You need to determine the total sales revenue your business generates for the period you are reporting. Receiving payments from your client for the already delivered services or products is unnecessary, and it will still be considered sales. Add up all the revenues you have written on your trial balance report, and then place the total revenues in your income statement’s first line.

Calculate Cost of Goods Sold:

The goods sold include direct costs such as direct materials, direct labor, and factory overheads. All of the costs used in the product’s selling were noted in the trial balance report, then added up and shifted to the list in the income statement under revenues.

Calculate the Gross Margin:

To calculate the gross profit, we subtract the total amount of goods sold from the total revenues, resulting in the total gross profit. The gross profit amount shows how much a business has earned profit from sales revenue.

Include Operating Expenses:

Gather up all the operating expenses in the trial balance report and then list the total amount in the income statement. The total operating expenses amount is listed in the income statement as selling and administrative expenses in the list.

Calculate your income:

Deduct the selling and administrative expenses amount from the gross profit amount, and it will result in the income generated before applying the tax rate. This income calculated is known as Earnings Before Taxes (EBT).

Include income taxes:

Multiply the given tax rate by the state by the pre-taxable income. List the calculated amount under the pre-tax income, known as Earning After Taxes (EAT).

Calculate Net Income:

For calculating total Net Income, the earnings after taxes are deducted from the earnings before taxes amount. The resulting figure is the Net Income, the profit amount your company has gained and carried on as Retained Earnings. Retained earnings further could be reinvested in your business or left as it is. Net Income is the final line in the Income Statement.

Finalize your Income Statement:

Now add the final touches to your Income Statement by placing a header with the business’s name and details and mentioning the period on which the Income statement has been reported.

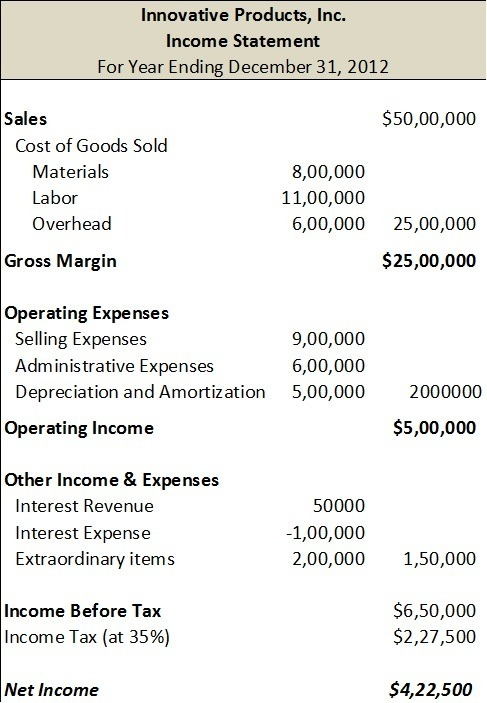

Example of Income Statement:

To clearly understand the Income Statement, we here present you an example taken from a company’s financial reporting.

Difference between a Balance Sheet and an Income Statement:

| Income Statement | Balance Sheet |

| An income statement is also known as a profit and loss statement, which means that it is used for reporting profits or losses of a business. | The balance sheet consists of assets and liabilities. |

| Income statements could be reported on a monthly, quarterly, or yearly basis. | The balance sheet gives a snapshot of a business’s/company net worth at a specific point in time. |

| Income statements tell about how much a business/company is efficient and what it has earned. | The balance sheet shows how much the business/company acquires liquid assets to fulfill its financial obligations. |

Browse our blog for more useful resources for your small business.

Related Articles:

Direct labor, time period, business owner, depreciation expense, resource, cost of sales, sales figures.