Retained earnings are found in the income statement and balance sheet both. Retained Earnings Statement is prepared separately also. In the balance sheet, retained earnings come under the heading of shareholder’s equity. In order to calculate retained earnings, you will have to subtract the total liabilities of a business from the total assets of a business; this amount will further be subtracted from common stock or equity capital; the answer you get is retained earnings.

Retained earnings are directly shown in the balance sheet so you can find them easily, but if you want to calculate them separately, then you can apply the following method while keeping the balance sheet in view:

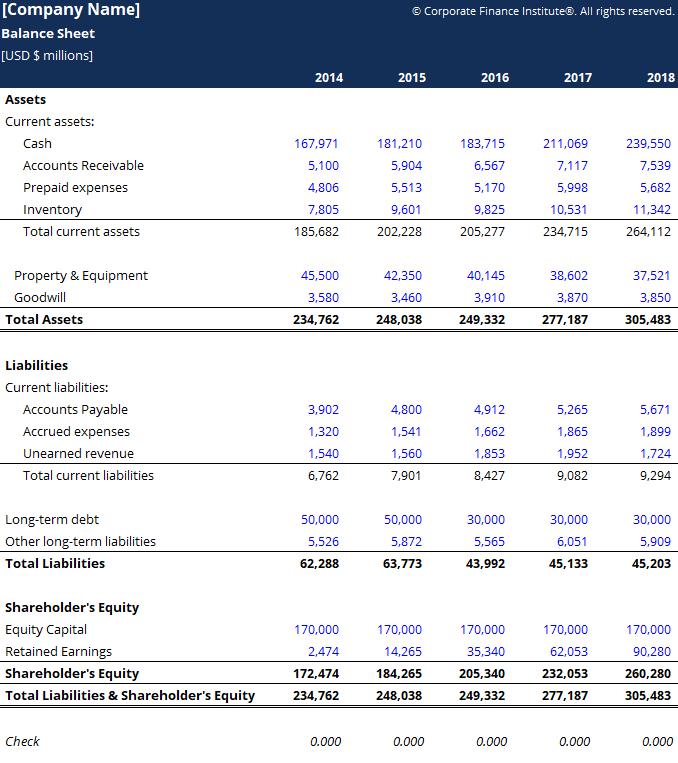

- Total assets of a company – Total liabilities of a company = Shareholder’s Equity

- Shareholder’s Equity – Common stock/Equity capital = Retained Earnings

This method can only be applied only if there are only two items in Shareholder’s Equity; equity capital and retained earnings. Other items can also be included depending on the complexity of a business’s balance sheet.

In this article, we will also discuss:

- How to prepare Retained Earnings Statement?

- What are Retained Earnings?

- How to Calculate Retained Earnings?

- How Dividends impact Retained Earnings?

- Are retained earnings a type of equity?

- Limitations of Retained Earnings.

- What are the three components of retained earnings?

How to prepare Retained Earnings Statement?

Retained earnings are found in the balance sheet easily when the balance sheet is prepared for each ending accounting period. But for a more clear view of the owners, the retained earnings statement is prepared for looking into the history of how a business has performed during the time. Retained earnings are the amount that is left after paying out dividends to stockholders, and the owners could reinvest this amount or payout to shareholders.

These are the following steps to prepare a Retained Earnings Statement:

Make the heading:

Prepare the heading of the document in the first three lines, that is:

- In the first line, write the name of the business or company.

- In the second line, add the title of the document you are preparing, which is ‘Statement of Retained Earnings.

- The third line is for mentioning the accounting period for which it is being prepared, e.g., ‘For the Year 2016’.

State the previous year’s balance:

After preparing the heading, now state the previous year’s retained earnings. Take out the previous year’s retained earnings from the previous year’s balance sheet. If you prepare your first statement of retained earnings, the beginning balance will be zero.

We consider that your previous year’s balance was $20,000. Then the balance will be written as:

Retained Earnings on January 01, 2016, $20,000

Add Net income:

Net income is taken from the Income Statement, so the income statement should be prepared before preparing this statement of retained earnings.

If we consider net income as $18,000, it will be added to the retained earnings.

Retained Earnings on January 01, 2016, $20,000

Add: Net income earned in 2016 $18,000

If the company faces a net loss, then the net loss will be subtracted from the beginning retained earnings amount.

- Subtract Dividend paid out to Stockholders:

Every business or company or business has its own policies for paying out dividends to its stockholders. The company already sets the dividend payout ratio.

For example, we say that the company pays dividends for 25% of its net income. Then the dividend amount will be subtracted from the subtotal.

Retained Earnings on January 01, 2016, $20,000

Add: Net income earned in 2016 $18,000

Subtotal: $38,000

Less: Dividends declared in 2016 $4,500

Dividends are always debited whether paid or not.

- Determine the total Retained Earnings:

After subtracting the amount of the dividends, you will get the final ending cost of retained earnings. The final amount is the total retained earnings for that year mentioned as per the balance sheet.

Retained Earnings on January 01, 2016, $20,000

Add: Net income earned in 2016 $18,000

Subtotal: $38,000

Less: Dividends declared in 2016 $4,500

Retained Earnings on December 31, 2016, $33,500

What are Retained Earnings?

Retained earnings are the profits that a business gains as the amount left as reserve not paid out for dividends, and then it’s the owner’s choice to reinvest the amount. The retained earnings overview the performance of a business and how it works over the period.

The amount of retained earnings can be used for launching new products or services, expanding business, paying off debts/loans, or paying out dividends.

How to Calculate Retained Earnings?

The formula for calculating Retained Earnings:

Retained Earnings = Beginning Retained Earnings + Net Income/Loss – Cash Dividends – Stock Dividends

How Dividends Impact Retained Earnings?

The distribution of dividends to shareholders can be in the form of cash or stock. Both forms can reduce the value of RE for the business. Cash dividends represent a cash outflow and are recorded as reductions in the cash account. These reduce the size of a company’s balance sheet and asset value as the company no longer owns part of its liquid assets.

Stock dividends, however, do not require a cash outflow. Instead, they reallocate a portion of the RE to common stock and additional paid-in capital accounts. This allocation does not impact the company’s balance sheet’s overall size, but it decreases the value of stocks per share.

Are retained earnings a type of equity?

Retained earnings are a type of equity, and are therefore reported in the Shareholders’ Equity section of the balance sheet. Although retained earnings are not themselves an asset, they can be used to purchase assets such as inventory, equipment, or other investments. Therefore, a company with a large retained earnings balance may be well-positioned to purchase new assets in the future, or to offer increased dividend payments to its shareholders.

Limitations of Retained Earnings:

As an analyst, the absolute figure of retained earnings during a particular quarter or year may not provide any meaningful insight, and its observation over a period of time (like over five years) may only indicate the trend about how much money a company is retaining. As an investor, one would like to infer much more such as how much returns the retained earnings have generated and if they were better than any alternative investments.

What are the three components of retained earnings?

The three components of retained earnings include the beginning period retained earnings, net profit/net loss made during the accounting period, and cash and stock dividends paid during the accounting period.

If you are looking for more helpful resources and guidance, then check out our resource hub.

Related Articles:

- How Much To Charge For House Cleaning?

- What is the Direct Write-Off Method?

- What are Legal Requirements Needed to Start a Business? 15 tips for Start-up

- What Is a Write-Off? Definition and Examples for Small Business

- How does a Payroll System work?

- What Are Billable Hours? Time Tracking Tips To Get You Paid

- What is the Cost of Goods Sold (COGS)? | Calculation & Explanation

- What Is a Deferral? It’s Expenses Prepaid or Revenue Not yet Earned

- How to Calculate Break-Even Point (BEP)?

- What are Debit and Credit? (Accounting Basics)

- How to Prepare a Trial Balance?