A T account represents a general ledger accounts graphical representation. The account name is above the “T” (sometimes along with the account number). Debits are shown on the left side of “T” and credits on the right side are shown of the “T”. At the bottom of the account is the overall total balance for each “T” account.

Typically, a number of T accounts are grouped together to show the full range of accounting transactions affected. The T account is a fundamental training tool in double entry accounting, showing how one side of an accounting transaction is reflected in another account. It is also quite useful for clarifying the more complex transactions. This approach is not used in single entry accounting, where only one account is impacted by each transaction.

How T Accounts are used?

The T account has two primary uses, which are:

To teach accounting, since it presents a clear representation of the flow of transactions through the accounts in which transactions are stored.

To clarify more difficult accounting transactions, for the same reason.

The T account concept is especially useful when compiling more difficult accounting transactions, where the accountant needs to see how a business transaction impacts all parts of the financial statements. By using a T account, one can keep from making erroneous entries in the accounting system.

For day-to-day accounting transactions, T accounts are not used. Instead, the accountant creates journal entries in accounting software. Thus, T accounts are only a teaching and account visualization aid.

Why Do Accountants Use T Accounts?

Accountants use T accounts in order to make double entry system bookkeeping easier to manage.

A double entry system is a detailed bookkeeping process where every entry has an additional corresponding entry to a different account. Consider the word “double” in “double entry” standing for “debit” and “credit”. The two totals for each must balance, otherwise there is an error in the recording.

A double entry system is considered complex and is employed by accountants or CPAs (Certified Public Accountants). The information they enter needs to be recorded in an easy to understand way. This is why a T account structure is used, to clearly mark the separation between “debits” and “credits”.

It would be considered best practice for an accounting department of any business (that is not using a single entry method of accounting) to employ a T account structure in their general ledger.

Example for T Accounts

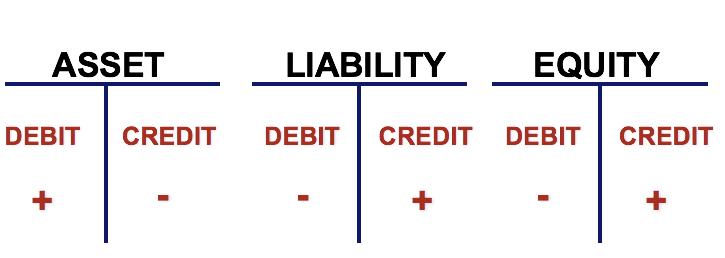

Let’s take a more in-depth look at the T accounts for different accounts namely, assets, liabilities, and shareholder’s equity, the major components of the balance sheet or statement of financial position.

For asset accounts, which include cash, accounts receivable, inventory, PP&E, and others, the left side of the T Account (debit side) is always an increase to the account. The right side (credit side) is conversely, a decrease to the asset account. For liabilities and equity accounts, however, debits always signify a decrease to the account, while credits always signify an increase to the account.

Where accounting meets business reality – what’s it all for?

When learning the accounting process, from debits and credits to double-entry, it’s easy to get lost in the process and miss the big picture.

What is this all for? Is this worth understanding if you aren’t an accountant?

Whether you are an accountant or a decision-maker the language of business finance is rooted in accounting. Whatever your role is in the business, it’s worth grasping the basics of this language.

Every transaction a company makes, whether it’s selling coffee, taking out a loan or purchasing an asset, has a debit and a credit. This ensures a complete record of financial events is tracked and can be accurately represented by financial reports.

The key financial reports, your cash flow, profit & loss and balance sheet are an organised representation of these fundamental accounting records. They are built from the ground up by these debits and credits. It’s these reports that you’ll be analysing to aid your decision-making process.

Your profit & loss organises your revenue and expense accounts whilst your balance sheet organises your asset, liability and equity accounts. The double entry process connects these reports together.

A single transaction will have impacts across all reports due to the way debits and credits work. So grasping these basics helps you delve into these reports and understand the financial story they tell.

Why Can’t Single Entry Systems Use T Accounts?

A single entry system of accounting does not provide enough information to be represented by the visual structure a T account offers. A single entry system records each of a company’s financial transactions as a single entry in a log, as opposed to a double-entry system which assigns each transaction to a category and records both a debit and credit for each.

T Accounts allows businesses that use double entry to distinguish easily between those debits and credits.

Related Articles: